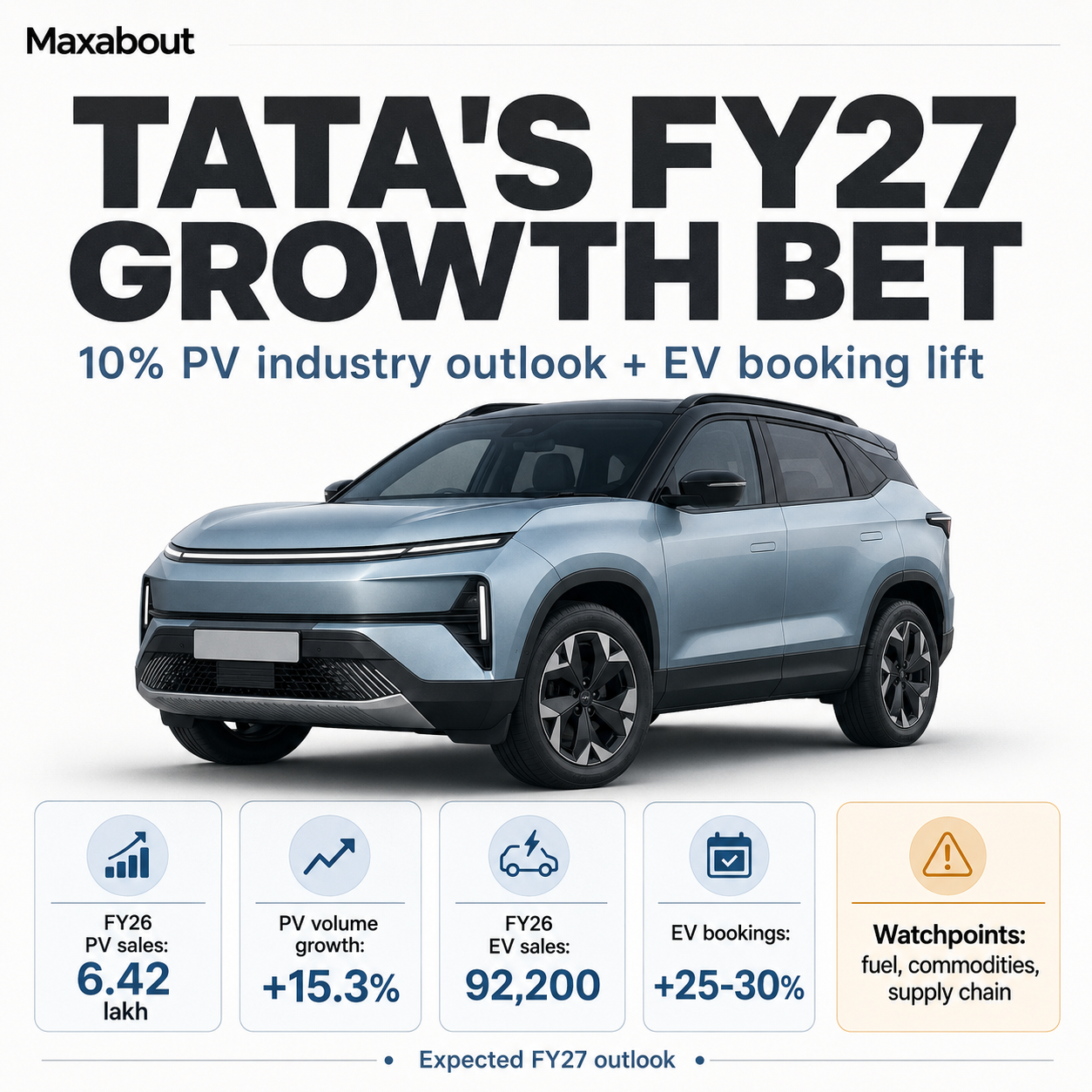

Tata Motors Forecasts 10% PV Industry Growth in FY27

The Indian passenger vehicle market is at a genuinely interesting moment right now. Not chaotic, not stagnant — just poised at a fork in the road where the next twelve months could define the industry's trajectory for years ahead.Tata Motors has put a number to that optimism: 10% growth for the PV i...

The Indian passenger vehicle market is at a genuinely interesting moment right now. Not chaotic, not stagnant — just poised at a fork in the road where the next twelve months could define the industry's trajectory for years ahead.

Tata Motors has put a number to that optimism: 10% growth for the PV industry in FY27. In plain terms, that means roughly 45,000 to 50,000 additional cars sold every month compared to current volumes. That is not a small shift. For everyday buyers, this kind of forecast quietly signals a few important things.

When manufacturers expect strong demand, they invest in new model launches, expand dealership networks, and sharpen pricing strategies to stay competitive. From what industry observers have noted, that typically works in the buyer's favour — more options, better feature packages, and occasionally even softer introductory pricing on new launches.

Waiting periods on popular models could also ease as production capacities get stretched to meet anticipated demand rather than reacting to it.

But here is where the story gets more layered. Tata Motors itself has flagged West Asia as a risk factor — geopolitical tensions in that region have a quiet but real effect on oil prices and freight costs, both of which eventually find their way into Indian showroom pricing. That tension between optimism and caution is worth examining carefully.

Understanding the 10% Growth Projection: Is Tata Being Realistic or Optimistic?

Let's put some actual numbers behind this forecast. The Indian passenger vehicle market currently sells somewhere in the range of 4.2 to 4.3 million units annually. A 10% growth on that base means the industry would need to add roughly 420,000 to 430,000 additional units in FY27. That is not a small ask. To put it in perspective, that incremental volume alone would be larger than the entire annual sales of several mid-sized automotive markets globally.

From what industry data suggests, FY25 growth was noticeably more modest — closer to the 4 to 5 percent range — after the strong post-pandemic rebound years had largely run their course. FY26 numbers, based on recent announcements and early estimates, appear similarly measured. So Tata projecting a sharp acceleration to 10% for FY27 does raise a fair question: is this grounded analysis or forward-looking confidence designed to reassure investors?

From what industry data suggests, FY25 growth was noticeably more modest — closer to the 4 to 5 percent range — after the strong post-pandemic rebound years had largely run their course. FY26 numbers, based on recent announcements and early estimates, appear similarly measured. So Tata projecting a sharp acceleration to 10% for FY27 does raise a fair question: is this grounded analysis or forward-looking confidence designed to reassure investors?

Honestly, it is probably both. Tata Motors has genuine market visibility that most outside observers lack — they see order pipelines, dealer inventory cycles, and financing trends in real time. That gives their projection some credibility. At the same time, a company forecasting strong industry growth also benefits commercially from that narrative, so the number deserves measured scrutiny rather than automatic acceptance.

Based on recent announcements from industry bodies, a range of 7 to 9 percent seems to be where most neutral observers are clustering their estimates for FY27. Tata's 10% sits at the optimistic end — not unreasonable, but not conservative either.

The West Asia Risk Factor: Why Global Tensions Can Slow Down Your Next Car Purchase

When analysts flag "West Asia risks," it can sound like abstract financial language. But the connection to your next car purchase is more direct than it appears.

The most immediate link is oil. India imports a significant portion of its crude from the Gulf region. Any sustained conflict or supply disruption there tends to push crude prices upward, which eventually shows up at fuel stations across the country. For someone buying an entry-level hatchback in Lucknow or a commuter two-wheeler in Coimbatore, a sharp rise in petrol prices changes the monthly budget calculation almost overnight. When fuel gets expensive, discretionary spending contracts — and a new vehicle is very much a discretionary purchase for most Indian families.

This effect hits hardest at the lower end of the market. A buyer in Nagpur stretching finances for a small car starts reconsidering when fuel costs climb alongside EMIs. That hesitation, multiplied across hundreds of thousands of buyers, can meaningfully slow down industry volume numbers.

Beyond fuel, there are supply chain dependencies worth understanding. Semiconductor components and certain raw materials move through financial and logistics networks with Gulf region exposure. Disruptions in that corridor can affect production timelines, even for vehicles assembled entirely in India.

There is also an export dimension. Indian automakers, including Tata, have been growing their presence in Middle Eastern markets. Prolonged instability in that region could compress export volumes, adding pressure to overall business performance even if domestic demand holds steady.

What's Actually Driving Growth: The Real Engines Behind India's PV Market

External risks aside, the domestic demand story feels genuinely solid. And when you look closely at where the growth is actually coming from, the 10% forecast starts making real sense.

The most significant shift is happening in cities like Indore, Surat, and Patna. Tier 2 and Tier 3 markets are no longer afterthoughts — they are increasingly the primary growth engine. Rising incomes, better road connectivity, and growing aspirations among younger buyers have created a wave of first-time car buyers who are skipping entry-level hatchbacks entirely and going straight to compact SUVs.

That single behavioural change has enormous implications. Even without dramatic volume growth, average selling prices climb significantly, pushing overall industry revenue higher. Manufacturers love this dynamic.

Easier financing has accelerated everything. Bank credit penetration in semi-urban India has improved considerably, making EMI-based ownership accessible to buyers who previously could not consider it. The electric vehicle segment is also contributing meaningfully, supported by government incentives that make the switch more financially attractive than before.

Then there is the broader SUV wave, which has fundamentally reshaped the market. From what industry observers consistently report, premiumisation is not slowing down — buyers are actively trading up, and that trend appears durable rather than cyclical.

Tata Motors' Own Stake in This Growth Story: Products, EVs, and Market Ambitions

Few brands stand to benefit more from this projected growth than Tata Motors itself. Over the past four to five years, Tata has transformed from a brand people were cautious about into one that genuinely excites buyers. The Nexon, Punch, Harrier, and Safari have each carved out strong positions in their respective segments — and that portfolio breadth is a real advantage.

Their EV story deserves special mention. Tata currently dominates India's electric passenger vehicle market, and here is where the West Asia tension angle becomes quietly interesting. If crude oil prices spike and fuel costs climb sharply, EV adoption could accelerate faster than anyone currently models. Tata, already holding significant EV mindshare, would be unusually well-positioned for exactly that scenario.

Based on official announcements, Tata has an aggressive product pipeline ahead — new electric platforms, refreshed existing models, and entries into segments they have not fully explored yet. That ambition looks credible given their recent execution record.

That said, the competition is fierce and honest acknowledgment matters here. Hyundai, Maruti Suzuki, and Mahindra are not standing still. Mahindra in particular has momentum that cannot be ignored right now.

From what industry analysts consistently highlight, Tata's biggest test will be service quality in smaller cities and flawless execution on upcoming launches. The growth story is real — but delivering it consistently across India's incredibly diverse market is where it gets genuinely difficult.

How This Forecast Affects You as an Indian Car Buyer in FY27

So Tata Motors expects the passenger vehicle industry to grow 10% in FY27. Sounds like a headline for boardrooms and analysts, right? But honestly, this forecast has real, practical implications for anyone planning to buy a car this year.

More brands chasing more buyers generally works in your favour. When the overall pie is growing, manufacturers tend to compete harder on pricing, features, and financing offers. You might not see dramatic price cuts, but expect more aggressive exchange bonuses, extended warranties, and free service packages — especially around festive season windows.

The flip side, however, is waiting periods. If demand genuinely accelerates toward that 10% growth target, popular models could see booking queues stretch again — similar to what happened post-pandemic. If you have a specific model in mind, locking in your booking early in FY27 rather than waiting could save you months of frustration.

For buyers in cities like Vijayawada, Rajkot, or Coimbatore, this growth cycle brings something arguably more valuable than price cuts — better dealership infrastructure. Brands investing in expansion tend to prioritise Tier 2 markets during growth phases, which means improved service centre access and actual spare parts availability locally.

But here is where the West Asia risk becomes personal. If regional tensions push crude oil prices significantly higher, fuel costs in India will climb. For anyone budgeting tightly, that changes the calculation entirely — a larger vehicle suddenly feels less practical. Smaller, fuel-efficient options could see renewed demand, and waiting for clarity on fuel prices before committing to a bigger purchase is genuinely sensible planning right now.

The EV Angle: Could Geopolitical Risk Actually Accelerate Electric Vehicle Adoption?

Here is a paradox worth thinking about. The same West Asia tensions that threaten India's broader economic stability could, ironically, become the strongest argument for electric vehicles that any policy document ever managed to make.

Indian buyers are extraordinarily sensitive to fuel prices. In the ₹8 lakh to ₹15 lakh segment especially, running costs matter as much as the sticker price. A Pune or Bengaluru commuter covering 40 to 50 kilometres daily in stop-and-go traffic is already spending significantly on petrol. If crude prices spike, that calculation shifts fast — and electric suddenly looks far more attractive than any government subsidy announcement ever made it feel.

From what daily EV users in cities like Bengaluru report, the running cost difference is already striking. Petrol at current prices can cost roughly ₹7 to ₹8 per kilometre for a typical hatchback or compact sedan. A comparable electric vehicle brings that down to under ₹2 per kilometre on home charging. Over a year, that gap is genuinely meaningful money.

Tata's existing lineup — the Nexon EV, Punch EV, and the upcoming Harrier EV — positions them well for exactly this moment. MG, Hyundai, and Mahindra are adding credible options too, which means buyers actually have real choices now, not just one or two token entries.

That said, charging infrastructure outside metro cities remains a honest concern. For someone in a smaller town or without home parking, an EV is still genuinely complicated — and pretending otherwise helps nobody.

Final Thoughts: Should You Be Confident or Cautious About the Indian Auto Market in FY27?

Honestly, both. And I think anyone giving you a clean, simple answer here is probably oversimplifying things.

Tata Motors' 10% growth forecast for FY27 is not wishful thinking — it reflects real structural demand. A growing middle class, improved financing access, younger buyers entering the market, and genuine product innovation across segments. These are not short-term noise. They are slow-moving, powerful forces that do not reverse easily.

But the West Asia situation deserves serious attention, not a footnote. Oil price volatility, remittance pressures, and supply chain sensitivities can collectively take the edge off even the most well-grounded forecast. External shocks have a way of humbling even the best projections — and this industry has learned that lesson before.

From everything I can observe, the underlying demand in India looks genuine. But if you are a buyer waiting for the "perfect moment," that moment may never arrive. Focus on your own financial readiness and the specific product that fits your life — not market sentiment.

India's automotive market right now is one of the most dynamic in the world. Real opportunities and real uncertainties exist side by side. That is actually what makes it worth watching closely.

Maxabout Team

Editorial Team

Specializes in: Automotive News, Reviews, Analysis

Want to read more automotive news?

Stay updated with the latest car launches, reviews, and industry insights.

Browse All News