India Auto Capex Push: ₹40,000 Crore FY27 Plans

Think about this for a moment. ₹40,000 crore. That is not a government budget figure or some abstract GDP statistic. That is the amount India's major automakers are planning to pour into their operations in a single financial year — FY27. To put it simply, if you stacked that in ₹500 notes, you woul...

Think about this for a moment. ₹40,000 crore. That is not a government budget figure or some abstract GDP statistic. That is the amount India's major automakers are planning to pour into their operations in a single financial year — FY27. To put it simply, if you stacked that in ₹500 notes, you would run out of space before you ran out of cash.

This is a number worth paying attention to, especially if you are someone who buys cars, follows the industry, or is simply curious about where Indian roads are headed over the next decade.

The names driving this capex wave are familiar. Maruti Suzuki, Tata Motors, Mahindra, Hyundai India — these are not fringe players making speculative bets. These are the companies that together account for the bulk of vehicles sold on Indian roads every single month. When they collectively commit to this scale of spending, it signals something bigger than quarterly earnings targets.

So why should you, as a car buyer or enthusiast, care? Because from what industry analysts are observing, this investment translates directly into more model choices, faster technology adoption, improved build quality, and potentially sharper pricing as competition intensifies.

This is not just capital expenditure on paper. It is a strong, coordinated signal about where Indian mobility is genuinely headed.

Who Is Spending What: Breaking Down the Major Players and Their FY27 Commitments

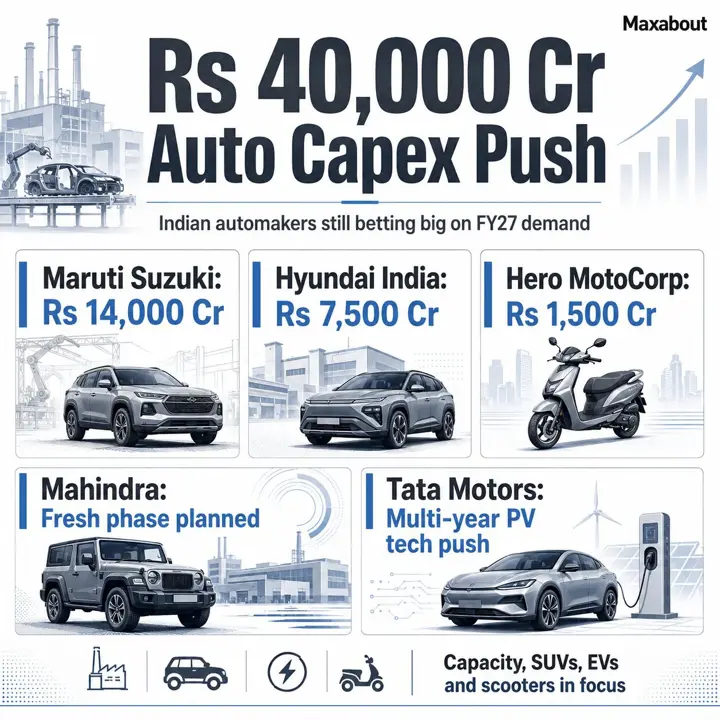

The ₹40,000 crore figure becomes far more interesting when you start looking at who is actually writing those cheques and what they plan to do with the money.

Maruti Suzuki is among the most aggressive spenders this cycle. The Kharkhoda plant in Haryana is central to their expansion story — a facility designed to significantly lift passenger vehicle output as demand continues outpacing supply in key segments. Beyond capacity, they are channelling serious resources into hybrid technology development, which appears to be their near-term answer to electrification.

Tata Motors is directing investment across two distinct fronts. Their EV platform development and battery localisation efforts represent one of the largest planned spends in the pure-electric space among Indian manufacturers. Simultaneously, their commercial vehicle division is receiving capital for both product refreshes and manufacturing efficiency improvements.

Tata Motors is directing investment across two distinct fronts. Their EV platform development and battery localisation efforts represent one of the largest planned spends in the pure-electric space among Indian manufacturers. Simultaneously, their commercial vehicle division is receiving capital for both product refreshes and manufacturing efficiency improvements.

Mahindra has committed heavily to its new electric SUV architecture. From what official announcements indicate, dedicated EV manufacturing lines and R&D infrastructure account for a significant portion of their planned outlay.

On the two-wheeler side, Bajaj and TVS are both directing capital toward electric platforms and export-ready manufacturing capacity — a combination that reflects both domestic ambition and global market thinking.

What is notable across all these commitments is the dual nature of the spending — nobody is betting exclusively on one powertrain technology. That measured approach tells its own story.

EVs, Hybrids, and ICE: Where Is the Money Actually Going?

The simple answer is: everywhere, but not equally. And that uneven split is actually quite revealing about how manufacturers read the Indian market right now.

Electric vehicle platforms and battery technology are getting the loudest attention — and a meaningful share of the capital. Battery pack localisation, cell chemistry research, and dedicated EV architectures are all drawing serious investment. The PLI scheme for Advanced Chemistry Cell batteries has added government weight behind this push, making domestic battery production financially attractive for the first time.

Hybrid powertrains sit in an interesting middle position. Strong hybrid technology — the kind that genuinely reduces fuel consumption rather than just adding a mild-assist motor — is receiving fresh investment, particularly from manufacturers who see it as a credible bridge for buyers not yet ready to commit to full electric.

But here is what does not get discussed enough: a substantial portion of this capital is still going into ICE upgrades. Emission compliance tightening, improved NVH refinement, better fuel efficiency calibration — these are not glamorous investments, but they are necessary ones. ICE vehicles still represent well over 90% of actual sales volumes in India.

Honestly, I think the tension here is real. Charging infrastructure outside major metros remains genuinely patchy. Price sensitivity is not a talking point — it is the dominant reality for most Indian buyers. The urban-rural divide in EV readiness is stark. Given all that, a spending split that still heavily favours ICE and hybrid development feels grounded in reality, even if it is less exciting to announce.

Whether manufacturers have found the right balance? That remains uncertain.

New Plants and Capacity Expansion: What It Means for Waiting Periods and Availability

If you tried booking a popular mid-size SUV anytime between 2022 and 2024, you already know the frustration. Waiting periods of six, eight, sometimes twelve months were not rare. Real buyers were losing money on extended insurance, missing registration deadlines, and simply watching prices inch upward while their booking sat in a queue. That experience left a genuine mark on buyer confidence.

This is where the ₹40,000 crore capex push becomes directly relevant to ordinary people — not just boardroom announcements. New plant investments and assembly line expansions should, in theory, ease exactly this kind of pressure. More capacity means faster order fulfillment, which means buyers regain some negotiating leverage they lost during the supply crunch years.

The realistic question, though, is whether new capacity will actually outpace demand growth. From what industry reports suggest, several manufacturers are planning facility expansions in Gujarat, Pune, and around the Chennai corridor. These regions already carry significant automotive infrastructure, which makes scaling faster and less complicated.

But here is the honest concern — demand has consistently surprised manufacturers on the upside. New capacity announced today takes eighteen to thirty-six months to operationalize meaningfully. If the market keeps growing at current rates, fresh capacity might simply get absorbed before waiting periods shrink noticeably. Buyers in the ₹12 to ₹20 lakh SUV segment especially should watch this carefully before assuming smoother availability by FY27.

Will This Investment Actually Make Cars More Affordable for Indian Buyers?

This is the question that matters most to someone standing in a showroom, staring at a price tag. Honestly, the answer is complicated — and anyone giving you a clean yes or no is oversimplifying.

Large capital investment can drive prices down, but not immediately and not uniformly. When manufacturers scale up domestic production, they unlock better economies of scale — more units spread fixed costs thinner. Add increased local component sourcing to that equation, and you reduce import dependency, which also means less exposure to rupee fluctuations against the dollar or euro. From what industry analysts consistently observe, higher localization levels typically shave meaningful costs off a vehicle's bill of materials over a two to three year horizon.

Platform sharing is another quiet cost reducer. When one architecture underpins four or five models across different segments, development and tooling expenses get distributed. That efficiency can — in theory — reach the buyer as competitive pricing.

But there are genuine counterforces. R&D recovery costs for new technology get baked into early pricing. Raw material inflation, particularly for steel and aluminium, has not been friendly recently. And premium features that buyers now expect — advanced safety systems, connected technology — add real cost regardless of manufacturing efficiency.

The honest picture: mainstream segments between ₹8 lakh and ₹18 lakh may gradually see sharper competitive pricing as capacity and localization improve. Electric vehicles, however, will likely remain premium for longer — battery costs and ecosystem development still carry significant investment recovery pressure that no amount of local assembly fully offsets yet.

The Export Angle: India as a Global Manufacturing Hub

Here is something worth paying attention to. Several automakers investing heavily in India right now are not purely chasing domestic demand. They are positioning India as an export base — building vehicles here and shipping them to markets across Africa, Southeast Asia, Latin America, and even parts of Europe.

This dual purpose actually matters for the domestic buyer, more than most people realize. When you are manufacturing for export to developed markets, quality standards cannot be negotiated. Global homologation requirements, stricter emission norms, and safety compliance demands from destination countries essentially force manufacturers to raise their overall production benchmarks — and those improvements flow into vehicles sold domestically too.

The government has been actively pushing this direction. Official targets to significantly grow India's auto export volumes have encouraged companies to treat Indian plants as genuinely world-class facilities rather than cost-reduction outposts.

But there is a real tension here worth acknowledging. Global platforms designed for international markets do not always translate perfectly to Indian conditions. Suspension tuning optimized for European highways, ground clearance suited to smooth urban roads abroad, or infotainment systems built around different connectivity infrastructure — these mismatches occasionally surface in vehicles that are technically excellent but feel slightly misaligned with how Indians actually drive.

From what reviewers and long-term owners consistently report, the best outcomes happen when manufacturers genuinely localize global platforms rather than simply transplanting them.

Risks and Realities: Can the Industry Actually Execute on These Plans?

Here is where honest thinking matters. A ₹40,000 crore capex announcement is genuinely exciting — but announcements and actual deployed capital are two very different things. India has seen this before. Large investment pledges made during optimistic cycles that quietly scaled back when market conditions shifted.

The global economic picture adds genuine uncertainty. If demand softens in key export markets, manufacturers recalibrate priorities fast. Domestic consumption, while resilient, is not immune to interest rate pressures and rural income volatility either.

Supply chains remain a real vulnerability. Semiconductors, battery-grade lithium, and cobalt are not sourced domestically at meaningful scale. Any disruption — geopolitical tension, shipping bottlenecks, export restrictions from supplier nations — can stall production lines regardless of how well a factory is built.

Then there is land acquisition and regulatory clearance. New greenfield plants in India rarely open on schedule. Environmental approvals, local resettlement concerns, and inter-departmental coordination have delayed projects by years historically.

Consumer EV adoption also remains slower than projections suggest. Charging infrastructure outside major metros is still patchy, and range anxiety is a legitimate concern, not just perception.

Perhaps the least discussed risk is talent. Building advanced manufacturing lines requires engineers, technicians, and process specialists trained in battery systems and software integration. That ecosystem in India is growing — but not yet at the scale this investment wave demands. The ambition is real. The execution gap deserves equal attention.

What Should Indian Car Buyers Do With This Information Right Now?

Here is the honest answer: don't freeze your decision waiting for a future that's still being built. Yes, the investment pipeline looks exciting. But factory announcements and actual showroom-ready products are separated by years, not months.

If you need a car today, the current market already offers genuine value. From what reviews consistently show, options across fuel, CNG, and entry-level EV segments are more competitive right now than they've been in years. Waiting indefinitely for "better" rarely works in your favour.

That said, if you're specifically eyeing an EV and live outside a major metro, a short wait might actually make sense. This capex wave will meaningfully improve service infrastructure in tier 2 and tier 3 cities — think Nagpur, Coimbatore, Lucknow — but realistically, that improvement is an 18 to 36 month story.

For everyone else, buy what solves your problem now. Don't time the market like it's a stock.

Looking ahead two to three years, I think Indian buyers will genuinely benefit — more platform choices, stronger after-sales networks, and real competition keeping prices grounded. The ambition behind this spending is credible. Just stay curious, stay patient where you can, and don't let excitement about tomorrow make today's perfectly good options invisible.

Maxabout Team

Editorial Team

Specializes in: Automotive News, Reviews, Analysis

Want to read more automotive news?

Stay updated with the latest car launches, reviews, and industry insights.

Browse All News