EV Two-Wheeler Makers Face Raw Material & AI Cost Hikes

Electric scooters have quietly gone from niche curiosity to everyday reality on Indian roads. You see an Ola S1, an Ather 450X, or a TVS iQube at almost every traffic signal in Bengaluru, Pune, or Hyderabad now. The Bajaj Chetak has made a genuine comeback. For millions of Indian buyers, the questio...

Electric scooters have quietly gone from niche curiosity to everyday reality on Indian roads. You see an Ola S1, an Ather 450X, or a TVS iQube at almost every traffic signal in Bengaluru, Pune, or Hyderabad now. The Bajaj Chetak has made a genuine comeback. For millions of Indian buyers, the question is no longer whether to go electric — it's which one to pick.

But right now, the companies building these scooters are facing serious headwinds. And those headwinds will almost certainly reach your wallet.

Two pressure points are converging at once. First, the global prices of raw materials — lithium, cobalt, and nickel — are climbing again. These aren't minor fluctuations. Battery packs are the single most expensive component in any electric two-wheeler, and every cost spike upstream eventually trickles down to the showroom price tag.

Second, manufacturers are under growing pressure to embed AI-driven features — smarter navigation, connected diagnostics, predictive maintenance — into their vehicles. That means heavy investment in software infrastructure, not just hardware. Building smart vehicles costs real money.

For the average buyer already calculating EMIs, worrying about charging points near their apartment, and wondering about resale value two years from now — this matters. A lot.

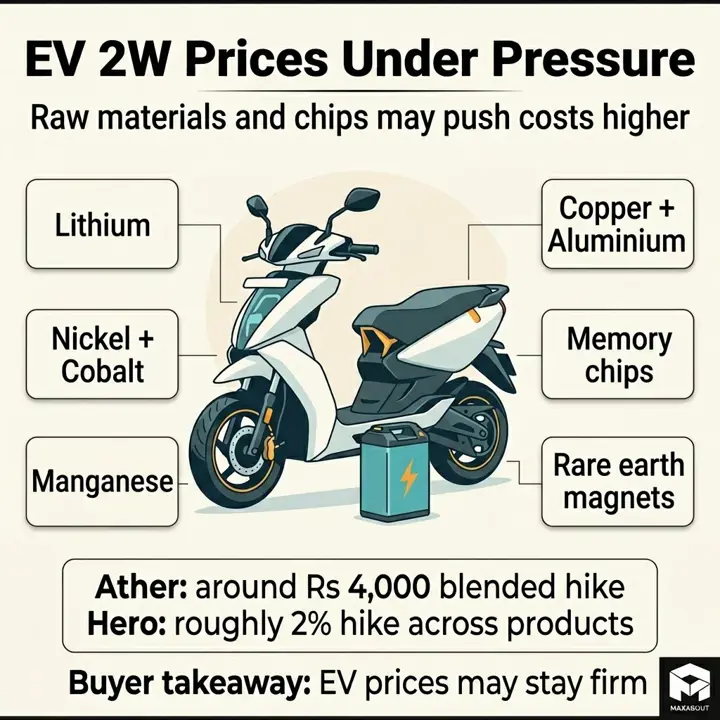

The Raw Material Problem: What Is Actually Getting More Expensive

Here is the uncomfortable truth about electric two-wheelers: the battery pack sitting under your seat accounts for roughly 30 to 40 percent of the entire vehicle's cost. And almost everything that goes into making that battery — lithium, cobalt, nickel, manganese, copper — India largely does not produce at scale. We import most of it.

That dependency creates a real structural problem. When global commodity prices move, Indian manufacturers feel it almost immediately. And right now, prices are moving in the wrong direction.

That dependency creates a real structural problem. When global commodity prices move, Indian manufacturers feel it almost immediately. And right now, prices are moving in the wrong direction.

Lithium, the backbone of most EV batteries, has seen significant price volatility over the past few years. Cobalt supply is heavily concentrated in the Democratic Republic of Congo, which introduces its own geopolitical uncertainties. Nickel markets were rattled badly after the Russia-Ukraine conflict disrupted supply chains. None of these are situations Indian manufacturers can simply negotiate their way out of.

Compounding the problem is surging global EV demand — particularly from China and the United States — which is competing for the same finite pool of raw materials. More buyers worldwide means more pressure on supply, and that pressure flows directly into procurement costs here.

Some manufacturers are responding by exploring lithium iron phosphate chemistry, commonly called LFP. It eliminates cobalt and reduces nickel dependence, which offers a meaningful cost buffer. From what industry observers note, LFP adoption is gradually increasing across the segment. But it is not a complete solution — lithium itself remains a bottleneck.

This is not a short-term disruption that resolves itself in one financial quarter. It is a structural challenge baked into how the global battery supply chain currently operates.

AI Infrastructure Costs: The Hidden Budget Pressure Nobody Is Talking About

Raw material volatility is the headline problem. But quietly running alongside it is another cost center that does not get nearly enough attention — the growing expense of building and maintaining AI infrastructure.

Today's electric two-wheeler is not just a vehicle. It is essentially a connected device on two wheels. Buyers now expect real-time diagnostics, theft alerts pushed directly to their phones, ride analytics, and battery health monitoring as standard fare. Features that felt premium two years ago are baseline expectations today. That shift has a price — and someone has to absorb it.

For larger players, spreading those server costs, data pipeline investments, and software engineering salaries across high volumes is manageable. For smaller Indian EV startups, it is genuinely punishing. They are competing in the same feature conversation while operating on far thinner margins.

Consider what over-the-air updates alone require — secure cloud infrastructure, version control, testing environments, round-the-clock monitoring teams. Then add AI-powered battery management systems that learn riding patterns to optimize range. Then smart navigation. The investment stacks up fast and never really stops.

The uncomfortable reality is that this R&D spend cannot simply be passed on to buyers. Indian consumers in the electric two-wheeler segment are acutely price-sensitive. A ₹3,000 to ₹5,000 price increase over a competitor can genuinely shift purchase decisions. So manufacturers absorb the cost, compress margins further, and hope scale eventually catches up.

It is, in effect, a technology arms race where the entry fee keeps rising.

How Indian EV Makers Are Responding: Strategies Worth Watching

Faced with this squeeze, manufacturers are not sitting still. The responses vary considerably — some companies are going deep on vertical integration, others are looking for partners, and a few are quietly rethinking where their revenue actually comes from.

The most talked-about move is local battery cell manufacturing. The government's Production Linked Incentive scheme has created real financial incentives to build domestic cell capacity, and several players have announced ambitions here. On paper, this makes complete sense — reducing dependence on imported cells from China or South Korea directly addresses the raw material vulnerability. The problem is timing. PLI benefits follow production milestones that can stretch across years, while material price spikes arrive without warning. The safety net exists, but it does not always open fast enough.

Supplier diversification is another strategy gaining traction. Rather than single-source agreements, some manufacturers are deliberately splitting orders across multiple vendors — including exploring lithium sources from Australia and South America as alternatives to China-linked supply chains. It adds procurement complexity, but the logic is sound.

Joint ventures for raw material sourcing are also emerging, where smaller manufacturers pool purchasing power to negotiate better terms. Individually, a company moving 8,000 units monthly has limited leverage with a major cell supplier. Collectively, that changes somewhat.

On the technology side, a few companies are exploring shared AI infrastructure partnerships rather than building everything independently. From what industry observers note, this is still early-stage thinking — but the economics of splitting compute costs across non-competing partners is genuinely attractive.

Perhaps the most interesting strategic shift involves software monetization. Rather than depending entirely on hardware margins, some manufacturers are experimenting with subscription-based features — connected vehicle services, extended battery analytics, navigation packages. The idea is to build a revenue stream that improves over time rather than one that gets pressured every time lithium prices move. Whether Indian consumers will consistently pay monthly fees for vehicle software remains an open question, but the direction is logical.

Execution, though, is the honest caveat here. India's regulatory environment, supply chain complexity, and infrastructure gaps have a way of stretching timelines that look clean on strategy slides. The intentions are credible. The follow-through is where it gets difficult.

What This Means for Electric Scooter Prices in India: Should You Wait or Buy Now?

This is the section most buyers actually care about. Strategy discussions are fine, but if you are standing at a showroom weighing an Ola S1 X or an Ather 450S against your budget, the real question is simple: will prices go up, and should you move now?

Honestly, the signals are not entirely comfortable. The ₹80,000 to ₹1.5 lakh segment — which covers the bulk of mainstream electric scooter purchases in India — is already operating on thin margins. Raw material pressure from lithium and cobalt costs, combined with growing AI infrastructure investments that manufacturers are quietly absorbing, creates a cost structure that cannot stay invisible forever.

Most analysts expect manufacturers to absorb short-term increases rather than immediately pass them on. Market share is too fragile right now. But sustained pressure over two to three quarters typically forces one of two outcomes — gradual price increases or quiet feature trimming in base variants. Neither is great news for budget-conscious buyers.

The FAME subsidy situation adds another layer of concern. Previous policy cycles already demonstrated how subsidy reductions translate directly into showroom price jumps almost overnight. That experience left a mark on how buyers should think about current pricing windows.

That said, the counter-argument deserves honest acknowledgment. Battery technology continues improving, and manufacturing efficiencies could partially offset raw material costs over time. If you are not in a hurry, waiting eighteen months is not irrational. But if a specific model fits your requirements today at today's price, that window may be narrower than it looks.

The Smaller Players vs. The Big Names: Who Is More Vulnerable?

Not every electric two-wheeler brand is facing these pressures from the same starting position. That distinction matters enormously — both for the industry and for anyone about to spend ₹1 lakh or more on a new vehicle.

TVS, Bajaj, and Hero Electric carry real advantages here. Decades of supplier relationships, diversified revenue streams, and established dealer networks mean they can absorb short-term input cost shocks without existential consequences. If lithium prices spike, TVS can negotiate differently than a four-year-old startup can. That is just the reality of scale.

Ola Electric and Ather sit in an interesting middle ground. Both have raised significant capital and have genuine technological credibility. But operating at thin or negative margins while simultaneously investing in AI-driven features and manufacturing infrastructure is a balancing act. A prolonged raw material squeeze could force difficult choices — between expansion and stability, between feature development and cost control.

Then there are the truly small players. Regional brands and recent entrants with limited funding face something closer to existential risk if input costs climb sharply. Indian automotive history offers uncomfortable precedents here. After FAME II subsidy restructuring, several smaller electric two-wheeler brands quietly reduced service operations or exited certain markets altogether, leaving buyers stranded on warranty claims.

This is not a reason to automatically avoid newer brands — some are genuinely innovative. But brand stability deserves a place in your purchase decision alongside range, features, and price.

The Long View: Is India's Electric Two-Wheeler Growth Story Still Intact?

Step back from the near-term noise, and the structural case for electric two-wheelers in India remains genuinely compelling. Fuel prices are not getting cheaper. Urban air quality in cities like Delhi, Pune, and Bengaluru continues pushing policy conversations toward stricter emissions frameworks. And frankly, the cost-per-kilometre advantage of electric riding still makes real financial sense for daily commuters.

Short-term headwinds — raw material price pressure, rising AI infrastructure costs — are real. But they do not fundamentally alter where this market is heading.

Two developments over the next three to five years could meaningfully change the cost equation. Solid-state battery technology, still maturing globally, promises higher energy density and improved thermal stability — critical for Indian summer conditions. Meanwhile, domestic lithium processing capacity is gradually expanding, which could reduce dependence on imported cell supply chains and moderate input cost volatility over time.

On the AI side, cloud infrastructure costs historically follow a predictable pattern — they fall as the technology scales. The same pressures manufacturers feel today on connected vehicle features will likely ease as compute becomes more commoditized.

India's two-wheeler market is simply too large and too price-sensitive to ignore electric mobility. The transition will have turbulent chapters. But the direction of travel looks clear.

Practical Takeaways for Indian Buyers Considering an Electric Two-Wheeler in 2025

So where does all of this leave you, the actual buyer standing in a showroom or scrolling through spec sheets at midnight? Here is my honest take: do not let the sticker price be your starting point. Calculate total cost of ownership. Factor in electricity costs, annual servicing, and — critically — battery replacement.

That last point deserves real attention. Ask the dealer directly: what does a battery replacement cost after the warranty expires? If they cannot give you a straight answer, that tells you something important about the brand's transparency.

Warranty terms vary significantly across manufacturers right now. Look for:

Battery warranty duration and the capacity retention clause — a warranty that covers only complete failure is nearly worthless

Whether service centers exist within a reasonable distance in your specific city, not just the nearest metro

OTA software update policy — confirm whether future updates are included or will eventually become subscription-based

On pricing, if a model you are considering appeals to you today, waiting may not work in your favor. Input cost pressures are real and near-term price revisions are plausible.

This is a genuinely complex moment in the market. But informed buyers who ask the right questions can still make decisions they will not regret twelve months from now.

Maxabout Team

Editorial Team

Specializes in: Automotive News, Reviews, Analysis

Want to read more automotive news?

Stay updated with the latest car launches, reviews, and industry insights.

Browse All News